Table of Contents

For twelve straight years, the average American credit score went up every single year without exception. Then 2025 happened — and the streak ended. The national average FICO score fell for the first time since 2013, slipping to 713. That number alone is not alarming. But the story underneath it absolutely is. America’s credit health is splitting in two, and which side you end up on will determine what you pay to borrow money for the rest of this decade.

If your credit score is between 600 and 749, you are part of a group that is quietly shrinking — and the direction people are moving in tells you everything about where the economy is really headed.

713

Avg US FICO score 2025, first drop in 12 yrs

48.1%

Americans now score 750 or higher

15%

Now in “poor” score range — up sharply

36.1%

Avg credit utilization — danger zone

$1.277T

Total US credit card debt — all-time record

Sources: FICO Credit Insights Report 2025, Experian 2026, VantageScore CreditGauge March 2026, Federal Reserve Bank of New York, LendingTree 2026

The 12-year streak that just ended — and why it matters

From 2013 all the way through 2024, the average American FICO credit score climbed steadily upward, rising from 691 to a record high of 716. That unbroken run of annual improvements reflected a genuine recovery from the Great Recession — Americans were paying down debt, opening fewer risky accounts, and building longer credit histories. Then 2025 arrived with a combination of pressures that no single factor can fully explain, and the streak snapped.

The national average FICO score ended 2025 at 713, a two-point decline from 2024 according to Experian’s September 2025 data. FICO’s own Credit Insights Report puts the figure at 714, still down from the record. VantageScore’s separate model — used by many lenders alongside FICO — sat at 701 as of March 2026, down one point from March 2025. Two different scoring systems, two different methodologies, same conclusion: American credit health softened in 2025 for the first time in over a decade.

A two-point drop sounds trivial. But the distribution shift underneath that average is anything but. 48.1% of Americans now score 750 or higher — the highest share ever recorded, up from 43.3% in 2019. Within that group, 24.8% score in the 800 to 850 exceptional range, also a record. Simultaneously, the percentage of Americans in the poor credit range grew to 15% in 2025. The middle is hollowing out. This is what economists call a K-shaped recovery — and your credit score is one of the clearest ways to see it happening in real time.

“The middle score range of 600 to 749 shrank from 38.1% of the population in 2021 to just 33.8% in 2025. More consumers moved into both the highest and lowest score brackets simultaneously.” — FICO Credit Insights Report, September 2025

Gen Z is getting hit the hardest — and here is the data that proves it

Gen Z consumers aged 18 to 28 saw the largest average FICO score decline of any generation in 2025, falling three points to an average of 678 according to Experian. That number sits at the low end of the “good” range — meaning millions of young Americans are one missed payment away from dropping into territory that will cost them significantly more on every loan they ever take. The reason is not reckless spending. It is student loans.

FICO data shows that 14.4% of consumers aged 18 to 29 experienced a score drop of 50 points or more year over year — compared to just 10.1% for the overall population. That is nearly 50% more likely to suffer a major score collapse than the average American. The culprit is the resumption of federal student loan repayments after pandemic-era pauses ended, combined with a job market that added fewer positions in 2025 than any year since the pandemic.

Millennials aged 29 to 44 averaged a 689 FICO score in 2025, down two points from 2024. Baby Boomers, meanwhile, were the only generation to actually improve — their average score rose one point to 747. Gen X held steady at 709 and the Silent Generation at 760. The older you are, the better your credit score is — and in 2025, the gap between generations widened rather than closed.

The perfect 850 club: As of March 2025, exactly 1.76% of Americans hold a perfect FICO score of 850 — the highest share since 2009 according to Experian. The state with the highest average score is Minnesota at 725. The city with the highest average is Seattle at 732. The lowest scoring city among America’s 50 largest is Detroit at 620, followed by Los Angeles at 529.

Credit card debt just hit an all-time record — and most Americans have no idea

Here is the number that should concern every American borrower: total U.S. credit card debt reached $1.277 trillion in Q4 2025 — the highest balance ever recorded since the Federal Reserve Bank of New York began tracking this data in 1999. That figure is $350 billion higher than the pre-pandemic record set in Q4 2019. In five years, Americans added more credit card debt than the entire GDP of many countries.

The average American now carries $6,360 in credit card debt, up from $5,900 in 2024. The average credit card APR in Q1 2026 is 21.00% for all accounts — and 23.75% for new card offers. At that rate, a borrower making only minimum payments on the average balance would take over 7 years to pay it off and spend roughly $3,610 in interest alone — on top of the original balance. Americans carrying balances over $10,000 jumped from 23% of cardholders in 2025 to 29% in 2026.

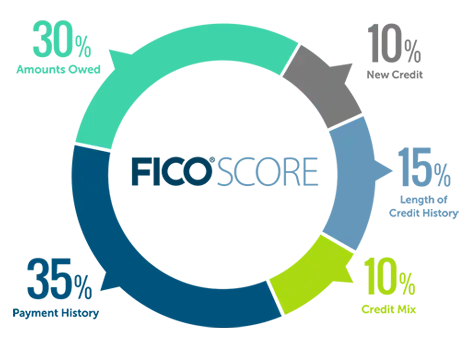

What makes this particularly alarming for credit scores is what it does to credit utilization. The average utilization rate — the percentage of available credit being used — surged from 21.3% in 2024 to 36.1% in February 2026, according to WalletHub’s analysis of TransUnion data. Credit experts consistently recommend keeping utilization below 30%. At 36.1%, the national average is now in the danger zone — and utilization is the second-most-important factor in your FICO score, accounting for roughly 30% of the calculation.

The payment hierarchy shift: Americans are now paying car loans before mortgages

One of the most surprising findings in FICO’s inaugural Credit Insights report — published in September 2025 — is a fundamental shift in how Americans prioritize their debt payments when money gets tight. For decades, the conventional wisdom was that Americans paid mortgages first, protecting their home above all other obligations. That hierarchy has now flipped.

Consumers are now 19% more likely to pay auto loans than mortgages, placing car payments at the very top of the payment priority list. Mortgages are 56% more likely to be paid than personal loans. Personal loans are 64% more likely to be paid than credit cards. And student loans rank at the absolute bottom — even among high-scoring borrowers who clearly understand the consequences of delinquency.

The reason for putting car loans first is not hard to understand: in a car-dependent country where many jobs require driving to work, losing a vehicle to repossession is often a more immediate threat to daily life than a mortgage delinquency. But the consequences for credit scores are significant. Bankcard delinquencies rose 48% since 2021. Mortgage delinquencies increased 58% since 2021, though still below pre-pandemic levels. Auto loan delinquencies climbed 24%.

“Debt delinquency expectations increased in December 2025 to the highest level since the beginning of the pandemic in 2020. Consumers expect a tougher job market and higher prices in 2026.” — Federal Reserve Bank of New York

The new FICO 10T is coming for your mortgage — what borrowers must know now

Beginning in 2026, the Federal Housing Finance Agency mandated that mortgage lenders use FICO 10T — the newest scoring model — for home loan applications. This is the biggest change to mortgage credit scoring in decades, and most borrowers have no idea it is happening. FICO 10T incorporates “trended data,” analyzing your payment patterns over the past 24 months rather than taking a single snapshot of your current balances. The difference matters enormously.

Under the old model, a borrower who always paid the minimum on credit cards looked identical to one who paid off their full balance every month — as long as their current balance and utilization were similar. Under FICO 10T, those borrowers score very differently. Consumers who consistently pay down balances will score higher. Those who make only minimum payments — even on time — may see lower scores than they expected. FICO research suggests that FICO 10T can boost thin-file consumers’ scores by 15 to 25 points through Buy Now Pay Later data when reported, but missed BNPL payments can damage scores equally fast.

For anyone planning to apply for a mortgage in 2026 or 2027, the implication is clear: your payment behavior over the past two years is now permanently on the record in a way it never was before. If you have been making minimum payments on credit cards, 2026 is the year to change that habit — not because of willpower, but because the math of what it will cost you on a 30-year mortgage has fundamentally changed.

What your credit score actually means for your loan rate right now

The practical impact of credit score on loan rates in 2026 is larger than at any point in the past decade, because the base rates are already elevated. When mortgage rates sit around 6.3%, the difference between a 760 credit score and a 680 credit score on a $400,000 home loan can be 0.5 to 1 full percentage point in interest rate — translating to a difference of $60,000 to $120,000 in total interest paid over the life of a 30-year mortgage. That is not a rounding error. That is a car, a child’s college education, or an entire retirement account contribution.

For personal loans, the spread is even wider. A borrower with exceptional credit in early 2026 might access personal loan rates around 8 to 10%. A borrower with fair credit — scores between 580 and 669 — may face rates of 20% or higher, nearly identical to credit card APRs. The whole point of a personal loan is typically to escape credit card interest, and borrowers with damaged credit scores often cannot access rates low enough to make that trade worthwhile.

Five things you can do right now to protect your credit score in 2026

Given everything the data shows about where credit scores are heading, the most important moves any borrower can make right now are concrete and measurable. Keeping credit utilization below 30% — ideally below 10% for the best scores — is the fastest lever most Americans can pull. A borrower sitting at 36% utilization who pays down balances to 29% can expect to see score improvements within one billing cycle, because utilization is reported monthly and has no memory of past high usage.

Checking your own credit report for errors is equally urgent. The Consumer Financial Protection Bureau has consistently found that a significant percentage of Americans have errors on their credit reports that are actively lowering their scores. Disputing those errors costs nothing, and the three major bureaus — Experian, Equifax, and TransUnion — are required by law to investigate disputes within 30 days. You are entitled to one free report from each bureau every year at AnnualCreditReport.com.

For borrowers with student loans, understanding exactly how your loans are being reported — and whether you are on an income-driven repayment plan that keeps your payments current — is critical in 2026. The FICO data showing 14.4% of young Americans experiencing 50-point score drops is almost entirely a student loan story. One missed student loan payment can stay on your credit report for seven years and affect every loan you apply for in that window.

Finally, for anyone planning a major purchase in the next 12 to 18 months, avoid opening new credit accounts unless absolutely necessary. Each new application triggers a hard inquiry, and opening multiple new accounts in a short window shortens your average account age — the third-largest factor in your FICO score. The best time to improve your credit is at least six months before you need it, not the week before you apply for a loan.

FAQ’s – Credit Score

What is the average credit score in the US in 2026?

The average FICO credit score in the United States is 713 to 714 as of 2025 data published in early 2026, according to Experian and FICO respectively. The average VantageScore 4.0 stands at 701 as of March 2026.

Is a 700 credit score good in 2026?

Yes. A 700 FICO score falls in the u0022goodu0022 range of 670 to 739. Borrowers at 700 can access most loan products, though they will not receive the best available rates. Scores of 740 and above unlock the most competitive rates from most lenders.

Why did average credit scores drop in 2025?

The primary drivers were the resumption of student loan payments, rising credit card utilization now at a national average of 36.1%, and increasing delinquency rates across credit cards and mortgages. The K-shaped economy means high scorers kept improving while lower scorers fell further.

What credit score do you need to get the best mortgage rate in 2026?

Most lenders offer their best mortgage rates to borrowers with FICO scores of 760 or higher. Scores between 700 and 759 typically qualify for good rates, while scores below 640 may face significantly higher rates or limited loan options.

How quickly can I improve my credit score?

Paying down credit card balances to below 30% utilization can show results within one billing cycle — typically 30 to 45 days. Disputing errors can take 30 days. Building a longer credit history and recovering from major negative items like missed payments takes 12 to 24 months of consistent on-time payment behavior.