Personal Loans: The Complete Guide for Americans in 2026

Whether you need money for a medical emergency, home improvement, debt consolidation, or a major life event — a personal loan can be one of the smartest financial tools available to you. But with dozens of lenders, varying interest rates, and different loan terms, knowing where to start can feel overwhelming.

This is your complete hub for everything personal loans in 2026. We cover how personal loans work, current rates, top lenders, how to qualify, and smart borrowing strategies — all in one place.

What is a Personal Loan?

A personal loan is an unsecured installment loan that allows you to borrow a fixed amount of money and repay it in equal monthly payments over a set period — typically between 1 and 7 years.

Unlike a mortgage or auto loan, a personal loan is not tied to any collateral. That means your home or car isn’t at risk if you struggle to repay. Instead, lenders approve you based on your credit score, income, and overall financial profile.

Key features of personal loans:

- Fixed loan amounts (typically $1,000 to $100,000)

- Fixed or variable interest rates

- Set repayment terms (12 to 84 months)

- Funds deposited directly to your bank account

- No restrictions on how you use the money

Personal Loan Statistics: Where America Stands in 2026

Personal loans have become one of the most popular financial products in the United States. Here’s a snapshot of where things stand right now:

- The average personal loan interest rate is 12.27% as of April 22, 2026, according to Bankrate Monitor data

- The average personal loan debt per borrower is $11,699 as of Q4 2025

- The lowest available personal loan rate among top lenders is 6.20% (for excellent credit borrowers)

- The typical APR range for personal loans is 8% to 36%

- 48.6% of personal loan borrowers use fintech/online lenders — the most popular option

- 21.6% use traditional banks and 20.3% use credit unions

- 3-year loan rates averaged 13.16% and 5-year loans averaged 17.52% as of mid-April 2026

- Borrowers with excellent credit have nearly a 90% approval rate, while those with poor credit have less than a 1% chance of approval

- Average personal loan rates are projected to hover near 12% throughout 2026

One important comparison: the average APR on new credit card offers is 23.77% as of February 2026. Personal loan rates — averaging 12.27% — are nearly 8 percentage points lower than credit card rates, making personal loans a significantly cheaper way to borrow money.

Current Personal Loan Rates by Lender Type — April 2026

Not all lenders charge the same rates. Where you borrow from matters significantly:

| Lender Type | Average APR |

|---|---|

| Online Lenders | 6.49% – 35.99% |

| Credit Unions | ~10.72% |

| Commercial Banks | ~12.06% |

| All Lenders Average | ~12.27% |

Source: Bankrate, TransUnion, Yahoo Finance — 2026

Online lenders consistently offer the most competitive starting rates and flexible eligibility requirements. Credit unions come in second, often offering rates below the national average for members. Traditional banks tend to have stricter requirements and higher average rates.

Personal Loan Rates by Credit Score

Your credit score is the single most important factor in determining your personal loan interest rate. Here’s what borrowers across different credit tiers can expect:

| Credit Score | Credit Tier | Expected APR Range |

|---|---|---|

| 720 – 850 | Excellent | 6.20% – 12% |

| 680 – 719 | Good | 12% – 18% |

| 640 – 679 | Fair | 18% – 24% |

| 580 – 639 | Poor | 24% – 30% |

| Below 580 | Bad | 30% – 36% |

Approval rates drop dramatically below a 640 credit score. Borrowers with scores below 580 have less than a 1% approval rate on most mainstream platforms.

The difference between excellent and fair credit on a $10,000 personal loan over 3 years is significant. At 8% APR, your monthly payment is approximately $313 and total interest paid is around $1,280. At 24% APR, your monthly payment jumps to approximately $392 and total interest paid rises to around $4,112 — more than three times as much.

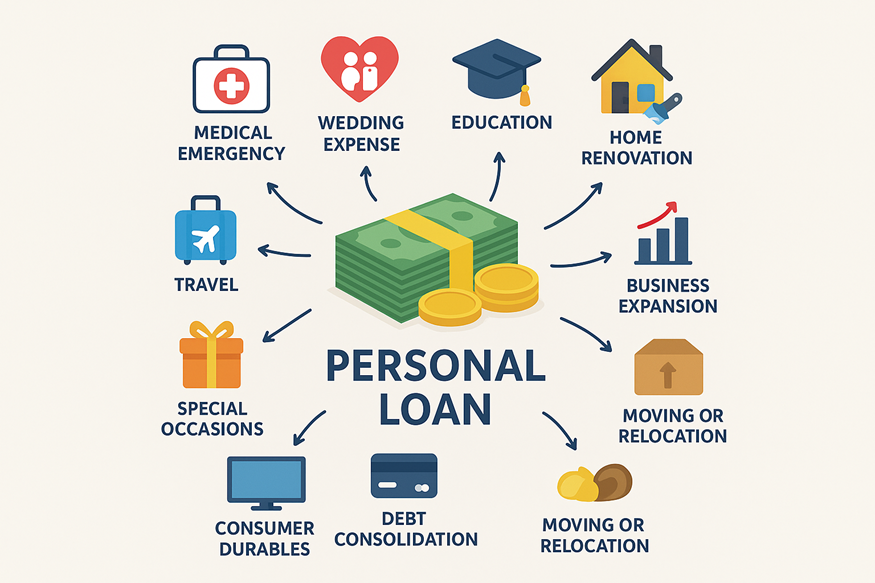

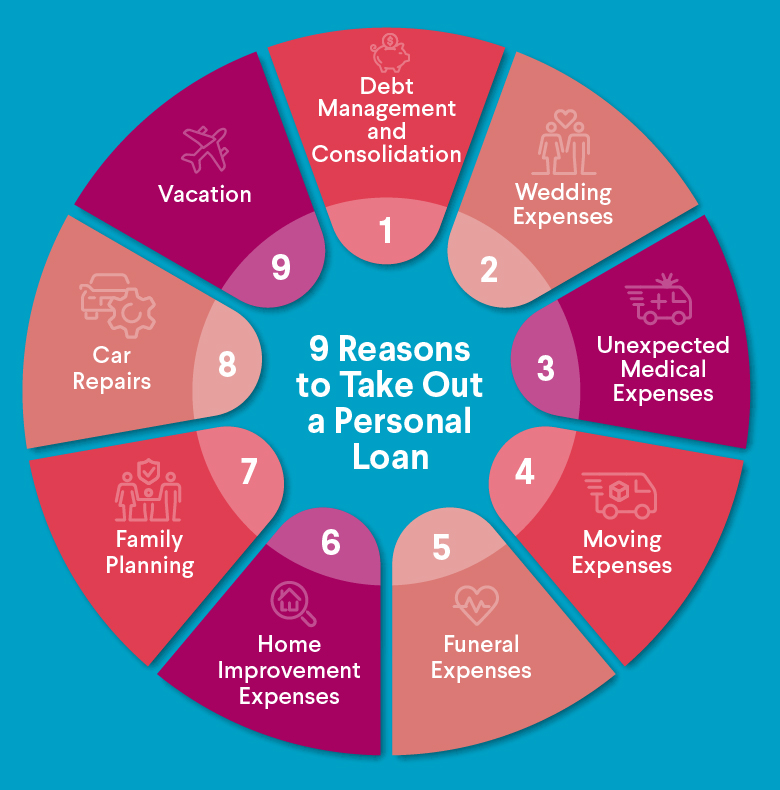

What Can You Use a Personal Loan For?

One of the biggest advantages of personal loans is flexibility. Unlike car loans or mortgages, there are virtually no restrictions on how you use the funds. Common uses include:

Debt Consolidation The most popular use of personal loans. By combining multiple high-interest credit card balances into one lower-rate personal loan, borrowers can simplify their payments and save significantly on interest.

Home Improvement From kitchen renovations to roof repairs, personal loans offer a fast alternative to home equity loans — with no risk to your property.

Medical Expenses Unexpected medical bills are one of the leading causes of financial stress in America. A personal loan can help you manage large medical expenses with predictable monthly payments.

Emergency Expenses Car repairs, emergency travel, urgent home repairs — personal loans can provide funds as quickly as the same day you apply with some lenders.

Major Life Events Weddings, funerals, moves, and other significant life events often come with large unexpected costs that a personal loan can help cover.

Education and Courses When federal student loans aren’t enough, personal loans can help cover tuition, certifications, or professional development costs.

Top Personal Loan Lenders in 2026

Here are some of the most competitive personal loan lenders available to American borrowers right now:

1. LightStream (Best for Excellent Credit)

- APR range: 6.99% – 25.49%

- Loan amounts: $5,000 – $100,000

- Terms: 24 – 144 months

- No fees, same-day funding available

- Best for: Home improvement, debt consolidation, major purchases

2. SoFi (Best for Good Credit)

- APR range: 8.99% – 29.49%

- Loan amounts: $5,000 – $100,000

- Terms: 24 – 84 months

- No fees, unemployment protection included

- Best for: Debt consolidation, home improvement

3. Upstart (Best for Fair Credit)

- APR range: 6.20% – 35.99%

- Loan amounts: $1,000 – $50,000

- Terms: 36 – 60 months

- Uses AI to evaluate non-traditional credit factors

- Best for: Borrowers with limited credit history

4. LendingClub (Best for Debt Consolidation)

- APR range: 8.98% – 35.99%

- Loan amounts: $1,000 – $40,000

- Terms: 24 – 60 months

- Direct payment to creditors available

- Best for: Consolidating credit card debt

5. Discover Personal Loans (Best for No Fees)

- APR range: 7.99% – 24.99%

- Loan amounts: $2,500 – $40,000

- Terms: 36 – 84 months

- No origination fees, 30-day money back guarantee

- Best for: Borrowers who want transparent pricing

6. Navy Federal Credit Union (Best for Military)

- Available to military members and families

- Competitive rates often below national average

- Flexible terms and member-focused service

- Best for: Veterans, active duty, and military families

How to Qualify for a Personal Loan

Lenders evaluate several factors when reviewing your personal loan application:

Credit Score Most mainstream lenders require a minimum score of 580–640. For the best rates, aim for 720 or higher.

Income Lenders want to verify you have stable, sufficient income to repay the loan. Most require proof of employment or self-employment income via pay stubs, tax returns, or bank statements.

Debt-to-Income Ratio (DTI) Your DTI is the percentage of your monthly income that goes toward debt payments. Most lenders prefer a DTI below 36%, though some accept up to 50%.

Employment History Stable, consistent employment strengthens your application. Most lenders prefer at least 2 years with the same employer, though this isn’t always required.

Credit History Beyond your score, lenders look at the age of your accounts, payment history, and any negative marks like collections or bankruptcies.

How to Apply for a Personal Loan: Step by Step

Step 1: Check Your Credit Score Pull your free credit report at annualcreditreport.com. Review it for errors that could be dragging your score down and dispute any inaccuracies.

Step 2: Decide How Much You Need Borrow only what you need. Every dollar borrowed costs money in interest. Calculate your exact need and stick to it.

Step 3: Prequalify with Multiple Lenders Most lenders offer a soft-pull prequalification that doesn’t affect your credit score. Use this to compare rates and terms across at least 3–5 lenders before committing.

Step 4: Compare APRs — Not Just Interest Rates The APR includes the interest rate plus any fees (origination fees, for example). Always compare APRs for a true cost comparison between lenders. Origination fees can be as high as 12% of your loan amount — a significant cost to factor in.

Step 5: Submit Your Application Once you’ve chosen a lender, complete the full application. You’ll typically need to provide your Social Security number, proof of income, employment information, and bank account details.

Step 6: Receive Funds Many online lenders fund within 1–3 business days. Some offer same-day or next-day funding for qualified borrowers.

Personal Loans vs. Other Borrowing Options

| Option | Average Rate | Secured? | Best For |

|---|---|---|---|

| Personal Loan | 12.27% | No | Flexible, multi-purpose |

| Credit Card | 23.77% | No | Short-term, small amounts |

| Home Equity Loan | ~8% | Yes (home) | Large home projects |

| HELOC | ~8.5% | Yes (home) | Ongoing home projects |

| 401(k) Loan | Prime + 1% | No | Last resort |

| Payday Loan | 300%+ | No | Never recommended |

Personal loans sit in a sweet spot — significantly cheaper than credit cards, and with no collateral risk unlike home equity products.

Smart Borrowing Tips for 2026

1. Improve your credit score before applying Even a 20–30 point improvement in your credit score can translate to a meaningfully lower interest rate. Pay down balances, correct errors on your credit report, and avoid new hard inquiries for 3–6 months before applying.

2. Shop multiple lenders within 14 days When multiple lenders perform hard inquiries within a short window, credit bureaus typically count them as one inquiry. Use this to your advantage and compare offers from at least three lenders.

3. Choose the shortest term you can afford Longer terms mean lower monthly payments — but significantly more total interest paid. If your budget can handle it, choose a 2 or 3-year term over a 5-year term.

4. Watch out for origination fees Some lenders charge origination fees of up to 12% of your loan amount. On a $10,000 loan, that’s $1,200 taken off the top before you receive your money. Always factor this into your comparison.

5. Have a repayment plan before you borrow Know exactly how you’ll make monthly payments before signing. Set up autopay — many lenders offer a 0.25% rate discount for doing so.

Frequently Asked Questions

Q: What is the minimum credit score needed for a personal loan?

Most mainstream lenders require a minimum score of 580–620. Lenders like Upstart use alternative data and may approve borrowers with lower scores. For the best rates (below 10%), aim for 720+.

Q: How fast can I get a personal loan?

Some lenders offer same-day funding. Most online lenders fund within 1–3 business days after approval. Traditional banks may take 5–7 business days.

Q: Will applying for a personal loan hurt my credit score?

Prequalification (soft pull) won’t affect your score. A formal application (hard pull) will cause a small, temporary dip — typically 5–10 points. This recovers within a few months with responsible use.

Q: Can I get a personal loan with bad credit?

Yes, but expect higher rates (24–36% APR) and stricter terms. Consider lenders like Upstart that evaluate non-traditional factors. A co-signer with strong credit can also help you qualify at better rates.

Q: What is the average personal loan amount in America?

The average personal loan debt per borrower is $11,699 as of Q4 2025, according to LendingTree data.

Q: Are personal loan interest rates going down in 2026?

Experts project personal loan rates to hover near 12% throughout 2026 — a slight decrease from 2025 but still significantly higher than pandemic-era lows. The Federal Reserve held rates steady in January 2026, limiting downward pressure on personal loan rates.

Final Thoughts

Personal loans are one of the most flexible and accessible financial tools available to American borrowers. With average rates around 12.27% in April 2026 — far below the 23.77% average credit card rate — they remain a smart option for debt consolidation, emergency expenses, and major purchases.

The key is to borrow smartly. Know your credit score, shop multiple lenders, compare APRs (not just interest rates), and choose a repayment term that balances affordability with total cost.

Whether you’re in New York, Chicago, Houston, or anywhere in between — LoanWiseUSA is here to help you find the right personal loan at the right rate.

Disclaimer: This page is for informational purposes only and does not constitute financial advice. Loan rates and terms are subject to change. Always verify current rates directly with lenders before making any borrowing decisions.