The US Economy 2026 is a study in contradictions right now. On paper, the numbers look reasonably solid. In people’s wallets, the story feels a lot more complicated. Here’s what the data actually says — and what it means for ordinary Americans.

Sources: U.S. Bureau of Economic Analysis (BEA), Bureau of Labor Statistics (BLS), U.S. Treasury

Where the U.S. economy actually stands

Let’s start with the headline number. U.S. GDP growth came in at 2.1% for 2025 as a whole — solid, but noticeably below the 2.8% the economy managed in 2024. The year ended on a weak note: Q4 2025 growth was revised all the way down to just 0.5%, dragged lower by the longest government shutdown in American history, which lopped roughly 1 percentage point off that quarter’s growth all by itself.

The good news? The economy bounced back. The advance estimate for Q1 2026 shows GDP rebounding to 2.0%, with government spending recovering at a 4.3% clip and business investment in equipment surging 10.4% — the fastest pace in nearly three years. A lot of that surge is tied to AI infrastructure spending, which has become one of the economy’s most powerful engines right now.

“Real consumer spending, which accounts for roughly two-thirds of U.S. economic activity, grew at just 1.6% in Q1 2026 — the slowest pace in recent memory.”

Consumer spending, the backbone of the American U.S. economy, is softening. Households are feeling the squeeze from tariff-driven price increases and still-elevated inflation. Personal consumption expenditures (PCE) inflation ran at 2.9% in 2025, comfortably above the Federal Reserve’s 2% target — and about half of that above-target inflation is directly attributable to tariffs passed through to consumers.

The labor market: a tale of two economies

Here’s where things get genuinely interesting — and a bit uncomfortable. The U.S. unemployment rate climbed from 4.1% at the start of 2025 to 4.4% by February 2026. That’s still below the 2012–2019 average of 5.5%, which means the labor market is not in crisis. But the direction of travel matters, and the trend has been consistently upward.

Job creation slowed dramatically. The economy added just 116,000 jobs across all of 2025 — the weakest annual performance since the pandemic era. Average monthly gains over the six months to January 2026 were a mere 14,000, compared to 122,000 per month throughout 2024. The culprits? A sharp decline in immigration cutting labor supply, plus firms holding back on hiring as they grapple with uncertainty from tariffs and AI adoption.

The income divide: Recent Dallas Fed research found that the top 20% of earners accounted for a record 57% of all consumer spending in the first half of 2025. The bottom 80% of households are struggling with inflation in a way that the headline numbers simply don’t capture.

Despite sluggish hiring, wage growth still outpaced inflation by around 1% in 2025 — a meaningful cushion for workers who kept their jobs. And layoffs remained historically low. The picture isn’t uniformly bleak; it’s uneven. Those who have stable employment are managing. Those looking for work are facing a much tighter market than the unemployment rate alone suggests.

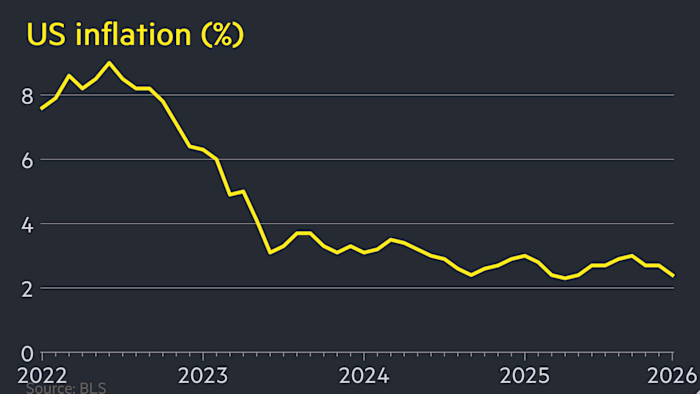

Inflation: better, but not beaten

The U.S. inflation rate has come a very long way from its June 2022 peak. Headline CPI was 2.7% as of December 2025 — down 6.4 percentage points from that peak. That’s a genuine achievement. But “better” is not the same as “solved.”

Core PCE inflation — the Fed’s preferred measure — sat at 2.7% for Q4 2025. Goldman Sachs estimates that without the tariff regime, inflation might have fallen as low as 2.3%, getting pretty close to the 2% target. Instead, tariffs added roughly 0.5 percentage points to the price level. With Middle East tensions now pushing energy prices higher, economists at EY expect headline PCE inflation to reach 3.0% by Q4 2026.

The Federal Reserve, for its part, has paused rate cuts while it waits for the economic data disruptions from the government shutdown to fully clear. Most forecasts expect three rate cuts in 2026, starting around June — but that timeline depends heavily on how inflation evolves.

AI and productivity: the bright spot nobody talks about enough

One of the most underappreciated stories in the American economy right now is productivity. Nonfarm business productivity surged in mid-2025: 4.1% in Q2 and 4.9% in Q3. That’s extraordinary. For context, the long-run average is closer to 1.5–2%.

AI investment is part of the story. Real investment in software rose nearly 16% at an annualized rate through Q3 2025. Data center construction spending reached $25.2 billion in Q3 alone, up 22% year-to-date. The tech sector has become the economy’s most reliable growth engine, even as manufacturing employment fell by 68,000 jobs across 2025.

Corporate profits tell the same story from a different angle: they surged by $247 billion in Q4 2025, with margins hitting a record 13.9% of GDP. The gains are real — but they’re accruing overwhelmingly to firms and shareholders rather than to workers broadly. Labor’s share of national income fell to a record-low 54.4% at end-2025.

“Labor productivity has grown at a 2.1% annualized pace since Q4 2019 — well above the 1.5% rate of the prior business cycle.”

What’s ahead: modest growth with real risks

The U.S. economic outlook for the rest of 2026 is cautiously positive but carries genuine downside risks. Deloitte’s Q1 2026 forecast puts real GDP growth at 2.2% for 2026, helped along by the statistical tailwind of strong late-2025 growth. Goldman Sachs is slightly more optimistic at 2.6%, citing expected tax cut benefits and easier financial conditions.

The risks are real though. The Middle East conflict has blocked the Strait of Hormuz, through which a fifth of global oil and LNG passes — driving energy prices higher and feeding into inflation. The Conference Board’s Leading Economic Index fell 0.6% in March 2026, signaling a slowdown ahead. Net migration is projected at just 321,000 in 2026 — a fraction of prior years — which means labor force growth is essentially stalling.

The stagflation concern: Stanford’s SIEPR warns that if inflation stays above 2% while unemployment keeps rising, the Fed faces a genuine dilemma. A repeat of the 1970s stagflation would be difficult to reverse once it takes hold.

The personal income picture offers some comfort: personal income grew 4.9% in 2025 across all 50 states and D.C., with every state seeing gains. The spread ranged from 6.9% in Hawaii to 3.2% in the District of Columbia. Real disposable income growth is expected to slow in 2026, but not collapse.

The bottom line

US Economy 2026 is resilient but strained. GDP is growing, productivity is rising, and corporate profits are at record levels. But inflation remains above target, job growth has slowed sharply, and the benefits of expansion are flowing disproportionately to top earners and capital holders. Consumer confidence dropped to recession-level readings in late 2025 for good reason — people’s lived experience doesn’t match the headline GDP numbers.

The U.S. economy has shown repeatedly that it can absorb shocks and adapt. The question for 2026 is whether AI-driven productivity gains and eventual rate cuts can lift growth broadly — or whether headwinds from geopolitical tensions, tariffs, and a tightening labor market will keep the recovery feeling hollow for most Americans.