Table of Contents

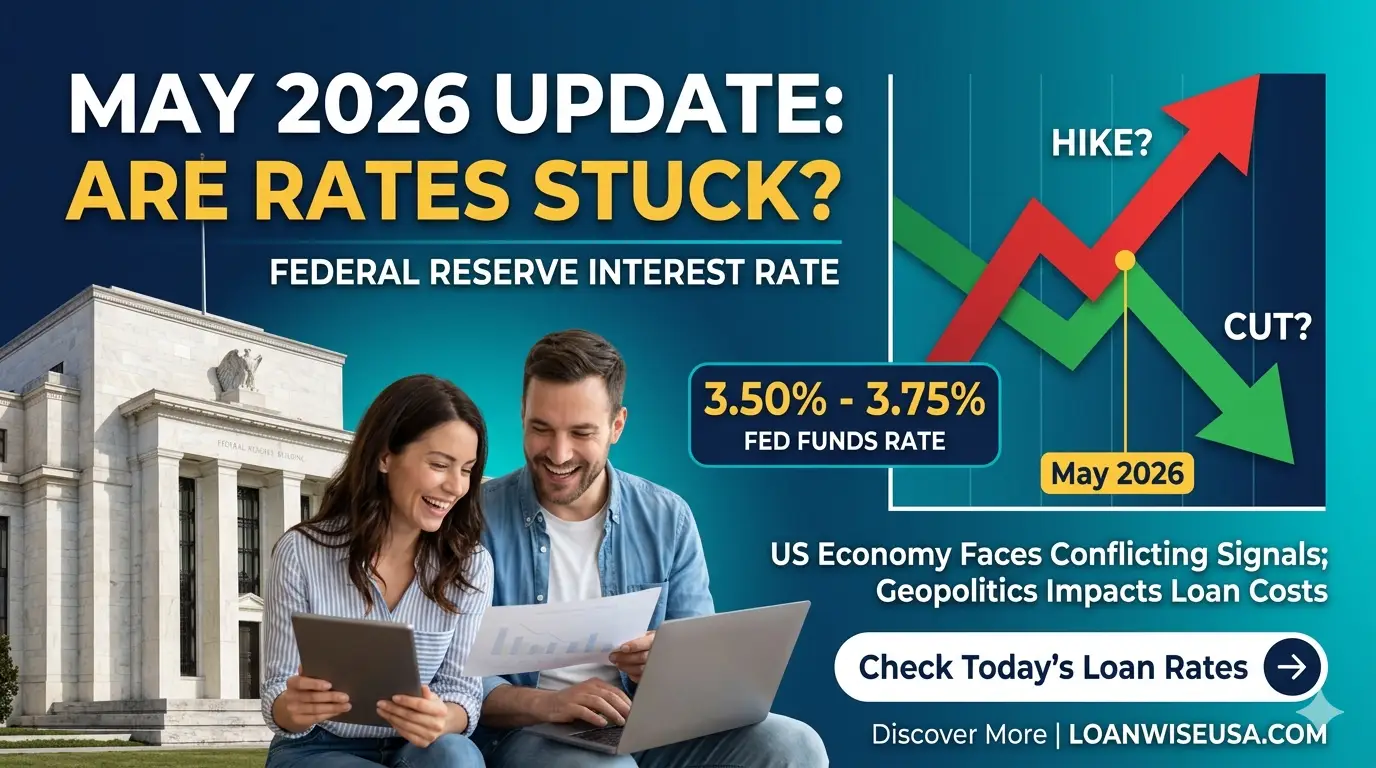

The American financial landscape is at a crossroads. As of May 2026, the Federal Reserve has once again held the benchmark interest rate in the 3.50% to 3.75% range. For millions of borrowers—from first-time homebuyers to small business owners—the “big pivot” toward lower rates remains tantalizingly out of reach.

But why is the Fed holding steady despite a cooling economy? The answer lies in a complex mix of geopolitical tensions, a leadership transition, and stubborn inflation and energy spikes.

The April-May 2026 FOMC Decision: A Deep Dive

In the most recent Federal Open Market Committee (FOMC) meeting on April 28-29, 2026, the decision to maintain rates was nearly unanimous. However, for the first time since 1992, we saw four significant dissents within the committee.

The Kevin Warsh Era Begins

A major shift is happening at the top. Jerome Powell has conducted his final press conference as Chairman. The Senate Banking Committee has advanced the nomination of Kevin Warsh to take the helm.

Warsh is known for favoring:

- A smaller Fed balance sheet.

- Less “forward guidance” (fewer hints about future moves).

- A “back-to-basics” approach focusing strictly on stable prices and maximum employment.

While Warsh has expressed a personal preference for lower interest rates in the current environment, his commitment to a leaner Fed suggests that the era of “easy money” may not return as quickly as some hope.

Why Federal Reserve Interest Rates Aren’t Dropping Yet

If you are waiting for a significant drop in your Federal Reserve interest rate, you need to understand the three primary “blockers” currently in the way:

1. The Iran Conflict & Energy Prices

Geopolitics is now a direct driver of your mortgage rate. The ongoing conflict in Iran has sent Brent crude oil prices soaring to a four-year high, touching $126 per barrel. This energy surge has “muddied” the inflation outlook, forcing the Fed into a “wait-and-see” mode to prevent a secondary inflation spike.

2. Stubborn Inflation vs. Growth

While Core PCE (Personal Consumption Expenditures) inflation had tempered to 3.0% by February 2026, the recent oil cost increases are threatening to push those numbers back up. The Fed’s dual mandate—keeping prices stable while maintaining low unemployment—is currently a balancing act.

3. Market Liquidity and the Balance Sheet

The Fed has stopped shrinking its bond holdings, which currently stand at approximately $6.6 trillion. To ensure banks have enough cash (liquidity), the Fed has actually started buying short-term Treasury bills again. This complex “reserve management” means the Fed is busy fixing the plumbing of the financial system rather than cutting rates for consumers.

Is Now the Best Time to Refinance?

Finding the right moment to lock in a loan can feel like chasing a moving target.

The Impact on Your Wallet: Mortgages, Personal Loans, and Refinancing

How does a stagnant Federal Reserve interest rate affect a typical user at LoanWiseUSA?

Mortgage Rates: The 6% Barrier

Mortgage rates are currently “bouncing around” the 6% mark. While they are far from the 8% peaks of late 2023, they aren’t dropping to the 5% range many expected.

- For Buyers: High rates plus record home prices are creating a “selective” market where supply is increasing, giving buyers more room to negotiate, but monthly payments remain high.

- For Sellers: Many are still “locked in” to their 3% pandemic-era rates, hesitant to sell and take on a new 6% loan.

Personal Loans and Credit Cards

Because the Federal Reserve interest rate remains high, APRs on credit cards and personal loans are still near historical highs. However, some banks have started slightly easing lending standards for consumer loans.

Forecast: When Will the Federal Reserve Interest Rate Finally Fall?

Predictions for the remainder of 2026 are split between “Steady” and “Slight Easing.”

- The Barclays View: Analysts now expect the Fed to maintain current rates throughout the entire year of 2026, abandoning previous predictions of rate cuts.

- The J.P. Morgan View: They see rates holding steady for the rest of 2026, with the possibility of a rate hike in 2027 if inflation isn’t controlled.

- The Bankrate View: Some analysts still hold hope that the 30-year fixed mortgage rate could fall to 5.5% to 5.7% by the end of the year, provided the economy cools further without a major recession.

Strategic Advice for Borrowers at Loan Wise USA

Given that the Federal Reserve interest rate is likely to stay high for longer, what should you do?

- Don’t Time the Bottom: If you find a home or a consolidation loan that fits your budget today, lock it in. Waiting for a “perfect” 4% rate in 2026 might be a losing game.

- Focus on Credit Health: In a high-rate environment, the gap between “Good” and “Excellent” credit can save you thousands. Lenders are becoming more selective.

- Watch the 10-Year Treasury: Mortgage rates often follow the 10-year Treasury yield more closely than the Fed’s daily rate. If yields dip, that is your signal to move.

Summary Table: May 2026 Economic Indicators

| Indicator | Current Status | Impact on Borrowers |

| Fed Funds Rate | 3.50% – 3.75% | High borrowing costs for all loans. |

| Inflation (PCE) | 3.0% (as of Feb) | Preventing major rate cuts. |

| Oil Prices | $126/barrel (Peak) | Upward pressure on interest rates. |

| 30-Yr Mortgage | ~6.1% (Avg) | Housing affordability remains pressured. |

Final Verdict: Is the Federal Reserve Interest Rate Still Your Enemy?

While a high Federal Reserve interest rate feels like a burden, it is also a sign of a resilient economy. Unemployment remains low, and consumer spending is stable. The key for 2026 is patience and precision.

At Loan Wise USA, we recommend staying tuned to our weekly Market Navigator. With a new Fed Chairman on the horizon and geopolitical shifts happening daily, the “best time to borrow” can appear in a flash.